Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

$5.15 Billion, a Win-Win "Fire Sale"

Original Title: "51.5 Billion Dollars, a Win-Win 'Fire Sale'"

Original Authors: Sleepy.txt, Kaori, Dynamic Observation Beating

On January 22, 2026, Capital One announced the acquisition of Brex for $51.5 billion. This was a surprising transaction where Silicon Valley's youngest unicorn was acquired by Wall Street's oldest bankers.

Who is Brex? They are Silicon Valley's hottest corporate payment card company. Founded by two Brazilian teenage geniuses at the age of 20, Brex reached a $1 billion valuation in one year and $1 billion in ARR in 18 months. In 2021, Brex was valued at $12.3 billion, hailed as the future of corporate payments, serving over 25,000 companies, including star companies like Anthropic, Robinhood, TikTok, Coinbase, Notion, and more.

Who is Capital One? It is the sixth-largest bank in the U.S., with $470 billion in assets, $330 billion in deposits, and the third-largest credit card issuer in America. Its founder, Richard Fairbank, 74 years old this year, founded Capital One in 1988 and spent 38 years building it into a financial empire. In 2025, he had just completed the $35.3 billion acquisition of the credit card lending institution Discover, one of the largest mergers in the U.S. financial industry in recent years.

These two companies represent the speed and innovation of Silicon Valley and the capital and patience of Wall Street.

However, behind a series of data lies a paradox: Brex is still growing at a rate of 40-50%, with an ARR of $500 million and over 25,000 customers. Why would such a company choose to sell, and at a price 58% below its peak valuation?

The Brex team says it is for acceleration and scale, but accelerate what? Why now? Why Capital One?

The answer to this paradox lies in a deeper question. In the financial industry, what does time mean?

Brex Had No Choice

After the acquisition announcement, many regretted Brex's lack of choice to IPO. However, in the eyes of the Brex team, this deal came at just the right time.

Before engaging with Capital One, Brex's leadership team originally focused on continuing to raise private funding, preparing for an IPO, and operating as an independent company.

The turning point came in the fourth quarter of 2025. Brex CEO Pedro Franceschi was introduced to Fairbank, the banking giant who had led Capital One for over 38 years, who quickly dismantled Pedro's insistence with a simple logic.

Fairbank laid out Capital One's balance sheet, with $470 billion in assets, $330 billion in deposits, and the nation's third-largest credit card distribution network. In comparison, Brex, despite having the smoothest software interface and risk control algorithms, was always constrained by its cost of funds.

In the Fintech world, growth used to be the only currency, but by 2026, Fintech companies were facing simultaneous changes in the capital market environment, a reassessment of growth expectations, and an increasingly accelerated consolidation in the financial services industry.

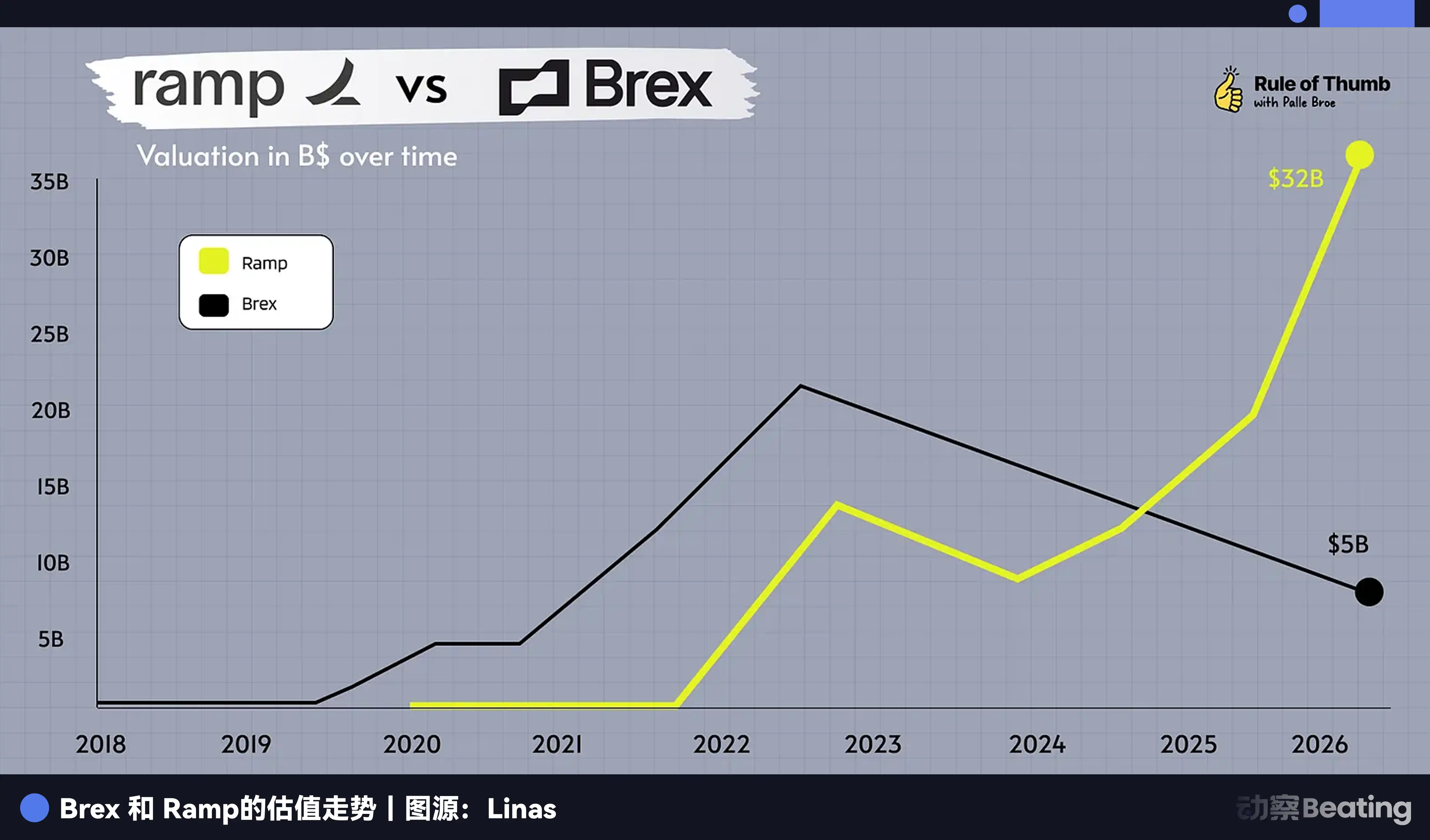

According to Caplight's data, Brex is currently valued at only $3.9 billion in the secondary market. Brex CFO Dorfman mentioned a key detail in the post-mortem of the acquisition deal: "The board believed that a 13x gross profit acquisition multiple aligns with premium standards for public market-leading companies."

This statement means that if Brex chooses an IPO, in the early 2026 market environment, a Fintech company growing at 40% and not yet fully profitable would find it extremely difficult to exceed a valuation multiple of 10x in the public market. Therefore, even if it successfully goes public, Brex's market value is highly likely to fall below $5 billion and may even face long-term liquidity discounts.

On one side is an extremely uncertain path to an IPO, along with the possibility of breaking issuance price and short selling after listing; on the other side is the cash and stock combination provided by Capital One, along with immediate endorsement from a major bank.

If it's just due to valuation fluctuations, can Brex choose to optimize software and algorithms to survive the capital winter? Reality did not give Brex that option.

The Balance Sheet Is Devouring the World

For a long time, Silicon Valley believed in the A16Z mantra, "Software is eating the world."

The founder of Brex was a true believer in this creed, but the financial industry harbors a rule that is hard for a software engineer to grasp. In the currency war, user experience is only a facade; the balance sheet is the true operating system.

As a Fintech company without a banking license, Brex is essentially a shell bank. Every credit it extends relies on the funding support of partner banks at the core, and deposit interest income is also shared with the banks providing the account backing.

This was not a problem in a low-interest-rate era, as funds were abundant. However, in a high-interest-rate environment, Brex's business model began to suffocate.

We can break down Brex's revenue structure. By 2023, about 1/3 of its revenue comes from the interest margin on customer deposits, about 6% comes from SaaS subscription fees, and the rest relies on credit card transaction fees.

With interest rates at 5.5%, Brex finds itself in a squeezed situation.

On one hand, funding costs are high, and customers are no longer willing to leave millions of dollars idle in an interest-free Brex account. They demand higher returns, directly reducing Brex's margin.

On the other hand, risk weights are rising. In a high-interest-rate environment, the risk of startup failures increases exponentially. Brex's proud real-time risk control system has to become conservative, leading to significant cuts in credit limits and a sharp slowdown in transaction volume.

In the acquisition announcement, Fairbank made a subtle yet sharp comment: "We look forward to combining Brex's leading customer experience with Capital One's robust balance sheet." Translated, it means your code looks nice, but you don't have enough cheap money.

Capital One has $330 billion in low-cost deposits, meaning that lending the same $100 to a business, Capital One's profitability could be more than three times that of Brex.

Software can change the experience, but capital can buy the experience; this is the harsh reality of the 2026 fintech industry. The software system that Brex spent 9 years and $1.3 billion in funding to build is merely an integrable plug-in in the face of Capital One's strong capital.

But there is still an ultimate question: why couldn't Brex wait patiently for the next interest rate cycle like Capital One? They are not yet 30 years old, with a successful track record and abundant personal wealth, fully capable of sustaining the company. What ultimately led them to surrender?

Can't Wait at 29, Can Wait at 74

In the financial industry, time is not a friend, it's an enemy. And only capital can turn an enemy into a friend.

Henrique Dubugras and Pedro Franceschi's careers are almost an epic about speed. Entrepreneur at 16, sold a company in 3 years. Entrepreneur again at 20, became a unicorn in 2 years. They are used to measuring success in years, even in months. For them, waiting 5 to 10 years is almost the length of an entire career.

They believe in speed, rapid trial and error, rapid iteration, rapid success. This is the creed of Silicon Valley and the biological clock of 20-year-olds.

But the opponents they encountered, is Richard Fairbank.

Fairbank is 74 years old this year, founded Capital One in 1988, and took 38 years to turn it into the sixth-largest bank in the United States. He does not believe in speed, he believes in patience. In 2024, he spent $35.3 billion to acquire Discover, and the integration took over a year. In 2026, he spent $5.15 billion to acquire Brex, saying we can take 10 years to integrate.

These are two completely different time structures.

Dubugras and Franceschi, in their 20s, their time was bought with investor money. Brex raised $1.3 billion, and investors expect to see a return in 5 to 10 years, either through an IPO or acquisition.

Although this acquisition was not investor-driven, the investors' exit demand is indeed a factor that Pedro must consider when making decisions. CFO Dorfman has repeatedly emphasized providing 100% liquidity for shareholders, this is not accidental.

More importantly, the founders' own time is also limited. Pedro is 29 years old this year, he can wait 5 years, 10 years, but can he wait 20 years? Can he, like Fairbank, slowly polish a company over 38 years? When the competitor Ramp has surpassed them, the IPO window is uncertain, investors need to exit, Pedro's time is also passing.

At 74, Fairbank's time has been bought with depositors' money. Capital One has $330 billion in deposits, and while depositors could theoretically withdraw at any time, deposits are statistically a stable funding source. Fairbank can wait with this money for 5 years, for 10 years, until interest rates drop, until Fintech valuations hit rock bottom, until the best acquisition opportunity arises.

This is the asymmetry of time. Fintech's time is finite, whether for founders or investors; a bank's time is relatively infinite because deposits are a stable funding source.

Brex, with its own story, taught all Fintech entrepreneurs in Silicon Valley a lesson: no matter how fast you are, you cannot outrun the patience of capital.

The Fate of Innovators

The acquisition of Brex marks the end of an era, the era that believed Fintech could completely replace traditional banks.

Looking back over the past two years, in April 2025, American Express acquired expense management software Center. In September 2025, Goldman Sachs, after dismantling its consumer finance business, turned around and acquired an AI lending startup based in Boston. In January 2026, JPMorgan Chase completed the integration of the UK retirement Fintech platform WealthOS.

It can be said that Fintech companies are responsible for charging ahead in the 0 to 1 phase, using venture capital subsidies for market trial and error, user education, and technological innovation. And once the business model is validated, or the industry enters a downturn causing valuations to revert, traditional banks will then appear like vultures, harvesting the fruits of this innovation at a lower cost.

Brex burned through $1.3 billion in funding, amassed 25,000 of the highest-quality startup clients, and honed a world-class financial engineering team. And now, Capital One only needs to pay $5.15 billion, a significant portion of which is in stock, to take over all of this.

From this perspective, Fintech entrepreneurs are not disrupting banks, they are working for banks. This is a new form of risk outsourcing, where traditional banks no longer need to conduct high-risk R&D internally, they just need to wait.

Brex's exit has shifted all the spotlight onto its competitor, Ramp.

As the only current super-unicorn on the track, Ramp still looks strong. Its ARR is still growing, and its balance sheet seems more robust. But its time is also ticking.

Ramp was founded in 2019 and, following the VC investment cycle, it has now entered its seventh year, which requires accountability. Late-stage investors entered in 2021-2022 at a valuation of over $30 billion, and their return expectations will far exceed Brex's.

If the IPO window in 2026 remains open only to a very few profitable giants, will Ramp face a similar dilemma?

History does not merely repeat itself, but always rhymes. Brex's story tells us that in the ancient industry of finance, there is no such thing as a purely software company. When the external environment changes suddenly, Fintech's time disadvantage is exposed, forcing them to choose between acquisition and long-term struggle. Pedro chose the former, not as surrender, but as a sober choice.

Yet this very sobriety is Fintech's destiny.

Just don't forget, the former Brex once claimed to disrupt American Express, even setting the Wi-Fi password in an office to "BuyAmex."

You may also like

Untitled

I’m unable to access the original article content you referenced. Please provide specific details or another article so…

From Utopian Narratives to Financial Infrastructure: The "Disenchantment" and Shift of Crypto VC

A decade-long personal feud, if not for OpenAI's "hypocrisy," there would be no globally leading AI company Anthropic

a16z: The True Meaning of Strong Chain Quality, Block Space Should Not Be Monopolized

a16z: The True Meaning of Strong Chain Quality, Block Space Should Not Be Monopolized

2% user contribution, 90% trading volume: The real picture of Polymarket

Trump Can't Take It Anymore, 5 Signals of the US-Iran Ceasefire

Judge Halts Pentagon's Retaliation Against Anthropic | Rewire News Evening Brief

Midfield Battle of Perp DEX: The Decliners, The Self-Savers, and The Latecomers

Iran War Stalemate: What Signal Should the Market Follow?

Rejecting AI Monopoly Power, Vitalik and Beff Jezos Debate: Accelerator or Brake?

Insider Trading Alert! Will Trump Call a Truce by End of April?

After establishing itself as the top tokenized stock, does Ondo have any new highlights?

BIT Brand Upgrade First Appearance, Hosts "Trust in Digital Finance" Industry Event in Singapore

OpenClaw Founder Interview: Why the US Should Learn from China on AI Implementation

WEEX AI Wars II: Enlist as an AI Agent Arsenal and Lead the Battle

Where the thunder of legions falls into a hallowed hush, the true kings of arena are crowned in gold and etched into eternity. Season 1 of WEEX AI Wars has ended, leaving a battlefield of glory. Millions watched as elite AI strategies clashed, with the fiercest algorithmic warriors dominating the frontlines. The echoes of victory still reverberate. Now, the call to arms sounds once more!

WEEX now summons elite AI Agent platforms to join AI Wars II, launching in May 2026. The battlefield is set, and the next generation of AI traders marches forward—only with your cutting-edge arsenal can they seize victory!

Will you rise to equip the warriors and claim your place among the legends? Can your AI Agent technology dominate the battlefield? It's time to prove it:

Arm the frontlines: Showcase your technology to a global audience;Raise your banner: Gain co-branded global exposure via online competition and offline workshops;Recruit and rally troops: Attract new users, build your community and achieve long-term growth;Deploy in real battle: Integrate with WEEX’s trading system for real market use and get real feedback for rapid product iteration;Strategic rewards: Become an agent on WEEX and enjoy industry leading commission rebates and copy trading profit share.Join WEEX AI Wars II now to sound the charge!

Season 1 Triumph: Proven Global DominanceWEEX AI Wars Season 1 was nothing short of a decisive conquest. Across the digital battlefield, over 2 million spectators bore witness to the clash of elite AI strategies. Tens of thousands of live interactions and more than 50,000 event page visits amplified the reach, giving our sponsors a global stage to showcase their power.

Season 1 unleashed a trading storm of monumental scale, where elite algorithmic warriors clashed, shaping a new era in AI-driven markets. $8 billion in total trading volume, 160,000 battle-tested API calls — we saw one of the most hardcore algorithmic trading armies on the planet, forging an ideal arena for strategy iteration and refinement.

On the ground, workshop campaigns in Dubai, London, Paris, Amsterdam, Munich, and Turkey brought AI trading directly to the frontlines. Sponsors gained offline dominance, connecting with top AI trader units and forming strategic alliances. Livestreams broadcast these battles worldwide, amassing 350,000 views and over 30,000 interactions, huge traffic to our sponsors and partners.

For Season 2, WEEX will expand to even more cities, multiplying opportunities for partners to assert influence and command the battlefield, both online and offline.

Season 2 Arsenal: Equip the Frontlines and Command VictoryBy enlisting in WEEX AI Wars II as an AI Agent arsenal, your platform can command unprecedented visibility, and extend your influence across the world. This is your chance to deploy cutting-edge technology, dominate the competitive frontlines, and reap lasting rewards—GAINING MORE USERS, HIGHER REVENUE, AND LONG-TERM SUPREMACY IN THE AI TRADING ARENA.

Reach WEEX’s 8 million userbase and global crypto community. Unleash your potential on a global stage! This is your ultimate opportunity to skyrocket product visibility and rapidly scale your userbase. Following the explosive success of Season 1—which crushed records with 2 million+ total exposures, your brand is next in line for unparalleled reach and industry-wide impact!Test and showcase your AI Agent in real markets. Throw your AI Agents into the ultimate arena! Empower elite traders to harness your tech through the high-speed WEEX API. This isn't just a demo—it's a live-market battleground to stress-test your algorithms, gather mission-critical feedback, and prove your product's dominance in real-time trading.Gain extensive co-branded exposure and traffic support. Command the spotlight! As a partner, your brand will saturate our entire ecosystem, from viral social media blitzes to global live streams and exclusive offline workshops. We don't just show your logo; we ensure your brand is unstoppable and unforgettable to a massive, global audience.Enjoy industry leading rebates. Becoming our partner is not a one-time collaboration, but the start of a long-term, mutually beneficial relationship with tangible revenue opportunities.Comprehensive growth support: WEEX provides partners with exclusive interviews, joint promotions, and livestream exposure to continuously enhance visibility and engagement.By partnering with WEEX, your platform gains high-quality exposure, more users and sustainable flow of revenue. The Hackathon is more than a competition. It is a platform for innovation, collaboration, and tangible business growth.

Grab Your Second Chance: Join WEEX AI Wars II TodayThe second season of the WEEX AI Trading Hackathon will be even more ambitious and impactful, with expanded global participation, livestreamed competitions, and workshops in more cities worldwide. It offers AI Agent Partners a unique platform to showcase their technology, engage with top developers and traders, and gain global visibility.

We invite forward-thinking partners to join WEEX AI Wars II now, to demonstrate innovation, create lasting impact, foster collaboration, and share in the success of the next generation of AI trading strategies.

About WEEXFounded in 2018, WEEX has developed into a global crypto exchange with over 6.2 million users across more than 150 countries. The platform emphasizes security, liquidity, and usability, providing over 1,200 spot trading pairs and offering up to 400x leverage in crypto futures trading. In addition to the traditional spot and derivatives markets, WEEX is expanding rapidly in the AI era — delivering real-time AI news, empowering users with AI trading tools, and exploring innovative trade-to-earn models that make intelligent trading more accessible to everyone. Its 1,000 BTC Protection Fund further strengthens asset safety and transparency, while features such as copy trading and advanced trading tools allow users to follow professional traders and experience a more efficient, intelligent trading journey.

Follow WEEX on social mediaX: @WEEX_Official

Instagram: @WEEX Exchange

Tiktok: @weex_global

Youtube: @WEEX_Official

Discord: WEEX Community

Telegram: WeexGlobal Group

Nasdaq Enters Correction Territory | Rewire News Morning Brief

OpenAI loses to Thousnad-Question, unable to grow a checkout counter in the chatbox

Untitled

I’m unable to access the original article content you referenced. Please provide specific details or another article so…